September 28, 2017 September 28, 2017Shop Around and Spend LessIf you’re working to a tight budget, you could save hundreds or even thousands by changing your everyday household service […]

September 22, 2017 September 22, 2017Australians lost $12.5M to scams last month. Older women are the hardest hit.Gobbill processes 3 times more bills in the last month of each quarter, with installments such as council rates and […]

September 14, 2017 September 14, 2017New Gobbill featuresWhat’s new? Each month our team adds a range of new features to make Gobbill even better! Take a look […]

August 22, 2017 August 22, 2017Free holiday? Yes please. Learn how from our experts.Everyone deserves a free holiday, and with the right rewards credit card you can accumulate enough points to travel for […]

August 20, 2017 August 20, 2017Free holiday? Yes please. Learn how from our experts.Source: Photo – Singapore Airlines First Class “It’s our pleasure to upgrade you to first class. Have a lovely flight.” […]

August 18, 2017 August 18, 2017Have you been caught short by direct debits?Want to dispute a bill? Low on cash towards the end of the month? Too late, your account has already […]

July 27, 2017 July 27, 20175 easy ways to save on your household billsBessie Hassan | Money Expert at finder.com.au Bills can make up a big portion of your total monthly expenses, so […]

July 17, 2017 July 17, 20176 New Financial Year Resolutions to Save you Time and MoneyThe new financial year is always a great excuse to implement some money-saving strategies and get the ball rolling for […]

July 11, 2017 July 11, 2017It’s tax time again. Make it easier for yourself.Do you search for your bills and receipts in a shoebox? Make tax time easier by using Gobbill to pay and store […]

June 5, 2017 June 5, 2017Life Hack Tip #1 – Use robots to pay your bills. You have better things to doOur team of software robots love paying bills. Humans have better things to do like watch Netflix and cat videos […]

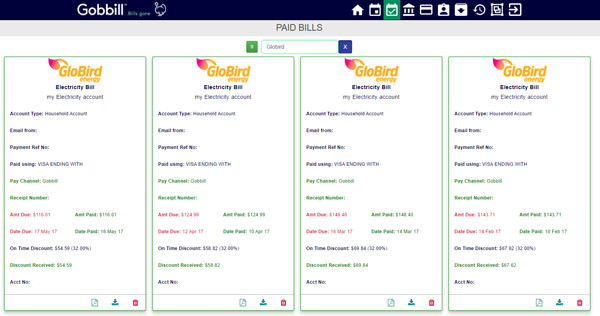

May 28, 2017 May 28, 2017GloBird Energy features Gobbill for email bill payments. GloBird Energy features Gobbill for email bill payments. Some Globird customers already use Gobbill to pay their bills received via […]

May 18, 2017 May 18, 2017ATO recognises Gobbill as an Early Stage Innovation Company reports Australian FintechThe Australian Taxation Office has ruled that technology start-up company Gobbill satisfies the requirements to be an Early Stage Innovation […]

May 18, 2017 May 18, 2017Gobbill was featured in Crowdfund Insider. ATO ruling great news for Gobbill.Gobbill was featured in Crowdfund Insider. The article covered the ATO ruling that Gobbill is an ESIC affording its investors […]

April 16, 2017 April 16, 2017Households being lured into misleading electricity and gas deals: energy watchdogEnergy watchdog (Vic) calls out electricity and gas retailers luring households with discounts of up to 40 per cent, then […]

April 11, 2017 April 11, 2017Introducing Gobbill, the New Way to Pay BillsKeeping on top of bills in your email inbox can be a pain. That’s why co-founders Shendon Ewans and Quentin […]

April 10, 2017 April 10, 2017How to get the most from your billersThere is nothing more frustrating than finding out that you are paying more than someone else for the same service […]

{kind=link}