Payroll tax affecting medical and health clinics.

June 12th, 2024 Posted by Gobbill Uncategorized 0 thoughts on “Payroll tax affecting medical and health clinics.”5 June 2024

Gobbill’s CEO Shendon Ewans hosted an event at NAB featuring Martin Goodrich of Goodrich Group as the key speaker about his experiences with payroll tax affecting medical and health practices.

Martin is a Chartered Accountant and has over 44 years’ experience in accounting and financial services. He acts as Chief Financial Officer and corporate advisor to many health and medical companies. He is currently the Chairman of Next Smiles Melbourne and partner in a new super dental clinic with his long-standing colleague, Dr Larry Benge.

Martin spoke about the issue from his perspective as a practice owner. This issue hits many business owners such as GP, dentists, physio, osteo, optometrists, pharmacists and other allied health and NDIS providers.

Then, it’s not just payroll tax but the flow on impacts of Superannuation, employer contributions, GST, PAYG, Workcover, leave entitlements and more..

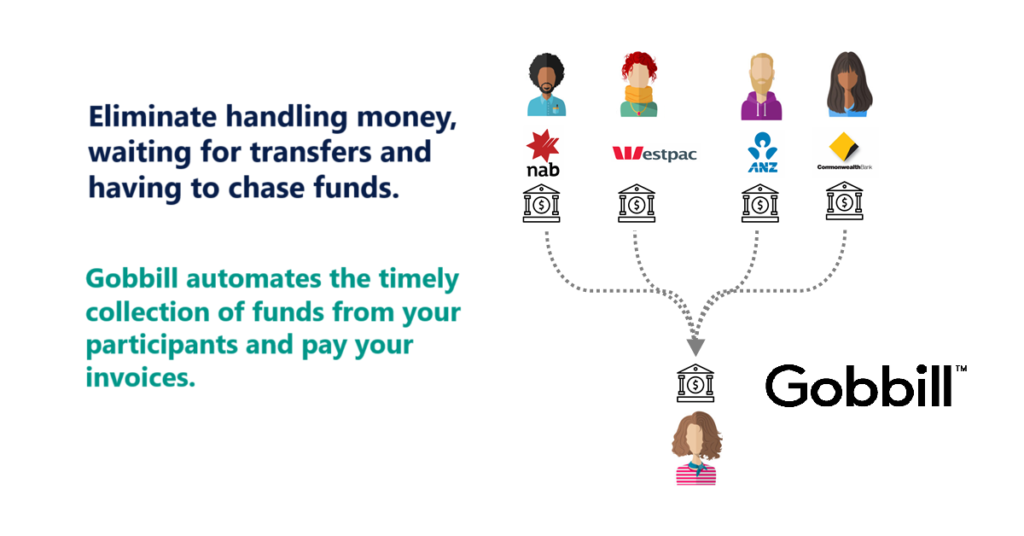

When reviewing your practice, consider also the money and payment flows. who controls the funds.

Often there are more admin steps and hassles. Gobbill automates the timely collection of funds from your clients’ bank accounts. It will improve your cashflow and significantly reduce administration & reconciliation time. Gobbill helps eliminate the hassle of managing money, waiting for transfers and having to chase funds.

Contact us to learn more or to discuss this topic further. We’re interested in your experience and what you hope to do. Email: [email protected]

Thank you NAB’s Laila Genitsaris for supporting the event.

About Gobbill

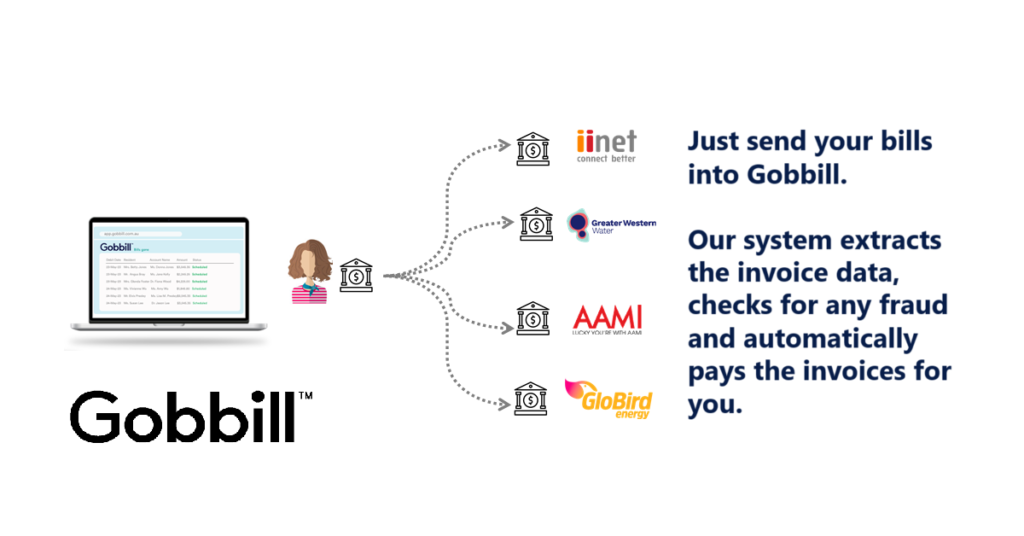

At Gobbill, we help many medical and health practices automate invoice payments. We streamline the movement of money and interactions between customers and suppliers. We reduce data entry, reconciliation and communication effort.

Gobbill can save up to 70% of time on accounts administration for business owners which in many cases can equate to around $30K per annum in savings.

The company was founded in Melbourne 9 years ago, is a compliant and regulated processor of money movement under ASIC and the NDIS Commission.

#medical #health #practices #GP #dentists #physio #osteo #optometrists #pharmacists #alliedhealth #ndis #payrolltax